Initiating coverage | Infrastructure

January 23, 2015

MBL Infrastructures

BUY

CMP

`442

Gearing-up for next level of growth

Target Price

`561

Strong Order inflows to lead to better execution: MBL Infrastructures (MBL), a

Investment Period

12 Months

specialist EPC player is expected to benefit from NHAI’s ~2,000km of EPC award

activity in the next 12 months. With economic revival, infra award activity across

verticals should catch-up. MBL has participated in projects worth `10,000cr.

Stock Info

Going by its past track record, of ~25% strike rate, MBL should report ~`2,500cr

Sector

Infrastructure

worth of new project wins in the next 12 months. We expect MBL’s order inflow to

Market Cap (` cr)

916

report ~13% CAGR over FY2014-17E, which is likely to be followed-up by

Net debt (` cr)

704

stronger execution. Accordingly, we expect MBL’s standalone entity to report a

strong ~18% top-line CAGR during FY2014-17E.

Beta

1.3

52 Week High / Low

464/100

~16% PAT CAGR during FY2014-17E: Stronger execution, benefits of backward

integration and better absorption of fixed costs, should help the standalone entity

Avg. Daily Volume

14,819

report a ~22% EBITDA CAGR during FY2014-17E (EBITDA margin to expand

Face Value (`)

10

107bp during the same period). Despite a strong EBITDA growth, higher interest

BSE Sensex

29,279

and depreciation expenses would restrict standalone PAT at ~16% CAGR during

Nifty

8,836

the same period, as per our estimation.

Reuters Code

MBLI.BO

BOT projects nearing completion: MBL has a portfolio of 5 BOT Road projects, of

Bloomberg Code

MBL@IN

which 4 are won on “Toll+Grant” or “Toll+Annuity” model. This, when coupled

with the fact that 4 of these projects are in the mineral belt region and are inter-

connected with no alternate roads, indicates that these projects could generate

impressive equity IRRs. With commencement of 4 BOT projects in FY2016-17, we

Shareholding Pattern (%)

can expect a possible easing in the balance sheet stress.

Promoters

46.7

Comfortable Balance Sheet: MBL is one of the Road developers with moderate

MF / Banks / Indian Fls

29.6

consol. D/E ratio of 1.8x. With 3 BOT projects nearing completion (to commence

FII / NRIs / OCBs

5.7

tolling in FY2016E) and 4th to commence operations in FY2017E, we expect

Indian Public / Others

18.1

consol. D/E ratio to increase to 2.7x by FY2017E. With Management clarifying

that it does not intend to add any new BOT projects to company’s portfolio till

FY2017E, we are confident that MBL’s D/E ratio would peak at 2.7x, which is

comforting.

Abs. (%)

3m 1yr 3yr

Sensex

9.4

38.5

72.3

Valuation: At CMP of `442/share, MBL is trading at FY2016E and FY2017E

EV/EBITDA multiple of 9.1x and 7.0x, respectively. Improved order inflow outlook

MBL

37.6

272.5

198.7

(with current bid pipeline of ~`10,000cr), strong profitability growth, and a

comfortable Balance Sheet strengthen our view that MBL is poised for re-rating

from here-on. We value BOT projects using PV of Free Cash Flows to Equity

shareholders to arrive at a value of `105/share (for all 5 of the BOT projects). We

have assigned 8.0x target P/E multiple to the standalone business to arrive at a

value of `456/share. On adding-up value of standalone entity and BOT projects,

we arrive at FY2017E sum-of-the-parts (SoTP) based price target of `561/share.

Given the 27% upside from the current levels, we initiate coverage on MBL

Infrastructures with a BUY rating.

Key Financials (Standalone)

Y/E March (` cr)

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Net Sales

1,343

1,754

2,019

2,453

2,857

% chg

30.6

15.1

21.5

16.5

Net Profit

55

75

85

100

118

% chg

35.8

12.9

18.4

17.6

EBITDA (%)

9.8

10.0

10.5

10.9

11.1

EPS (`)

32

43

41

48

57

P/E (x)

14.0

10.3

10.8

9.1

7.8

P/BV (x)

2.0

1.7

1.4

1.2

1.1

RoE (%)

15.1

17.6

15.2

14.4

14.8

RoCE (%)

16.6

19.3

17.5

16.5

16.5

Yellapu Santosh

EV/Sales (x)

0.9

0.7

0.8

0.7

0.7

022 - 3935 7800 Ext: 6828

EV/EBITDA (x)

9.2

7.0

7.5

6.8

6.0

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Initiating coverage | MBL Infrastructure

Investment Argument

Order Inflow outlook improves, gives better revenue

visibility

In a poor award activity environment during FY2010-14, captive orders from BOT

projects helped MBL clock a 36% CAGR in its order inflows. Taking into account

the new government’s thrust on the Infra sector, and with economic indicators

showing signs of revival; we expect revival across Infra award environment to

catch-up from here on.

Post amendments to the Land Acquisition Law, NHAI is gearing up to have a

strong award activity in 4QFY2015E-FY2016E. We expect NHAI to award

~4,000km of road projects in the next 12 months. Of these, ~2,000km would be

through the EPC route. With MBL’s Management clarifying that the company would

not be bidding for BOT projects, it can be estimated on this basis that MBL would

only bid for ~2,000km of EPC road projects.

The Management also highlighted that the company has bid for projects worth

~`10,000cr, which are currently at different bidding stages. If we look at the last

5 years’ historical win rate of 20-40%, coupled with slightly lower bidding intensity,

we are comforted that MBL is likely to report ~`2,500cr (indicating 25% strike rate

assumption) worth of project wins in the next 12 months.

Our order inflow growth assumption captures (1) resumption in award activity from

State PWDs/ NHAI Road projects, (2) award activity from DFC (Dedicated Freight

Corridor) space, and

(3) uptick in award activity from Metro, Industrial

Construction as well as Building & Housing Construction space. Accordingly, we

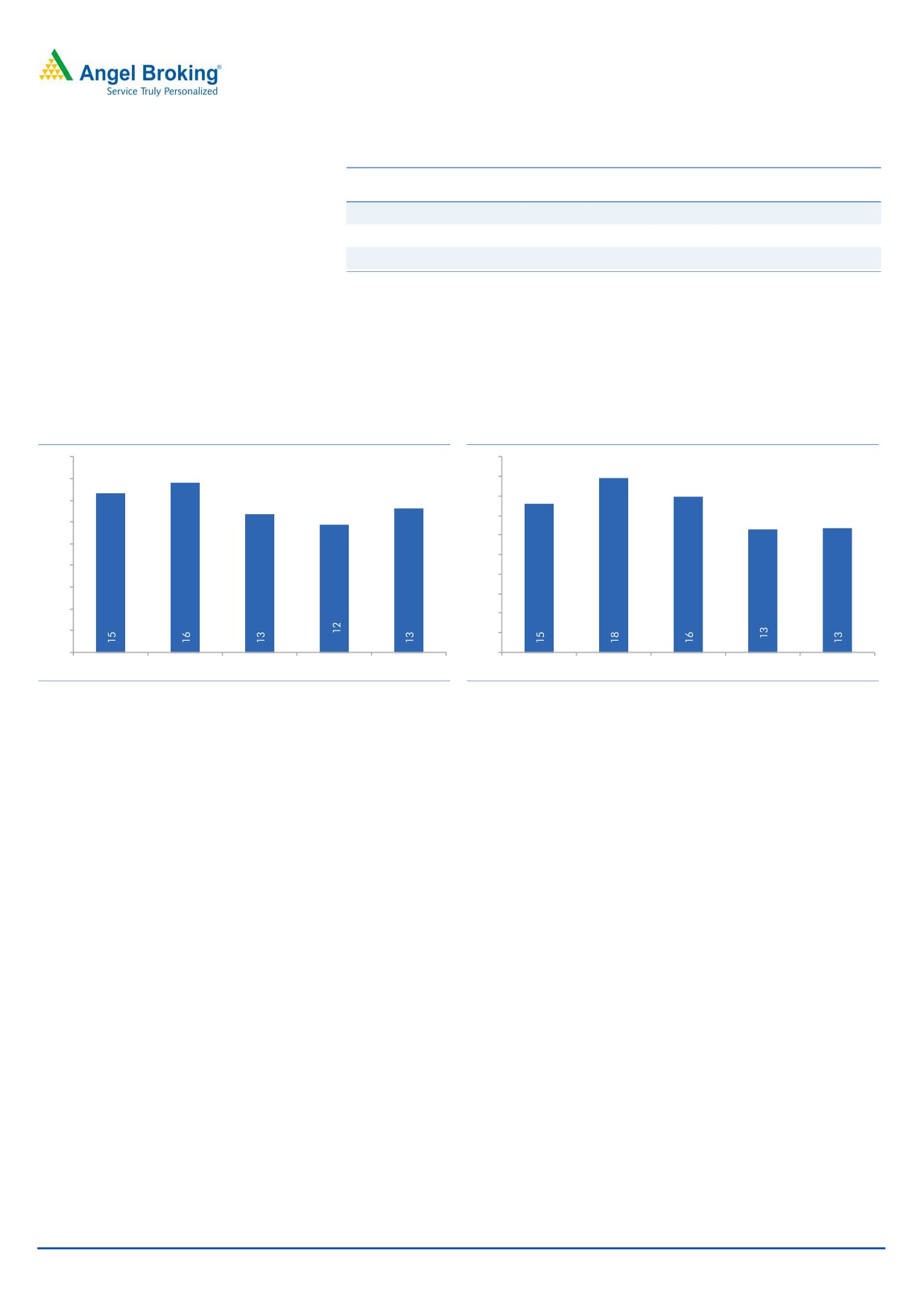

expect ~13% CAGR in MBL’s order inflows during FY2014-17E.

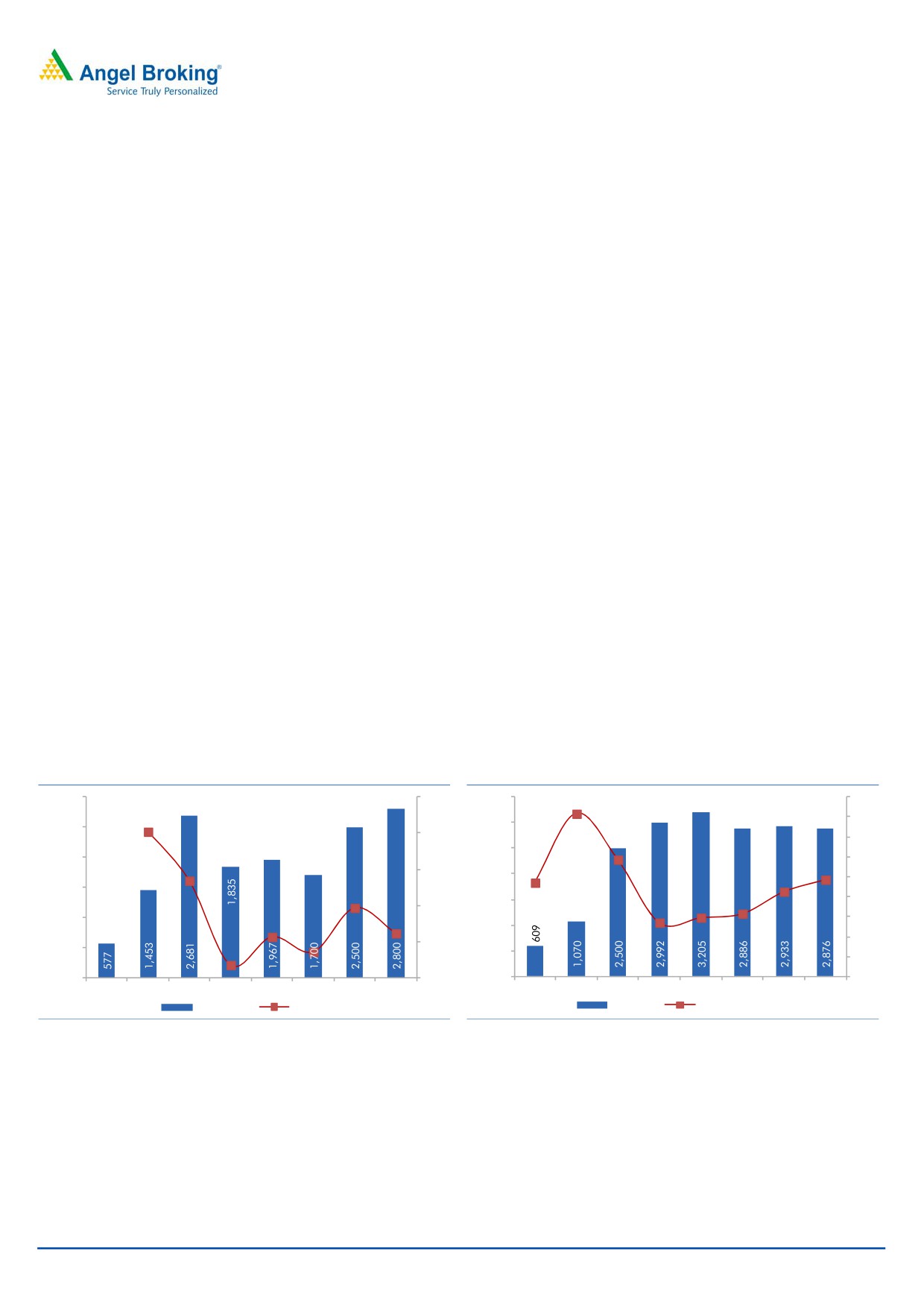

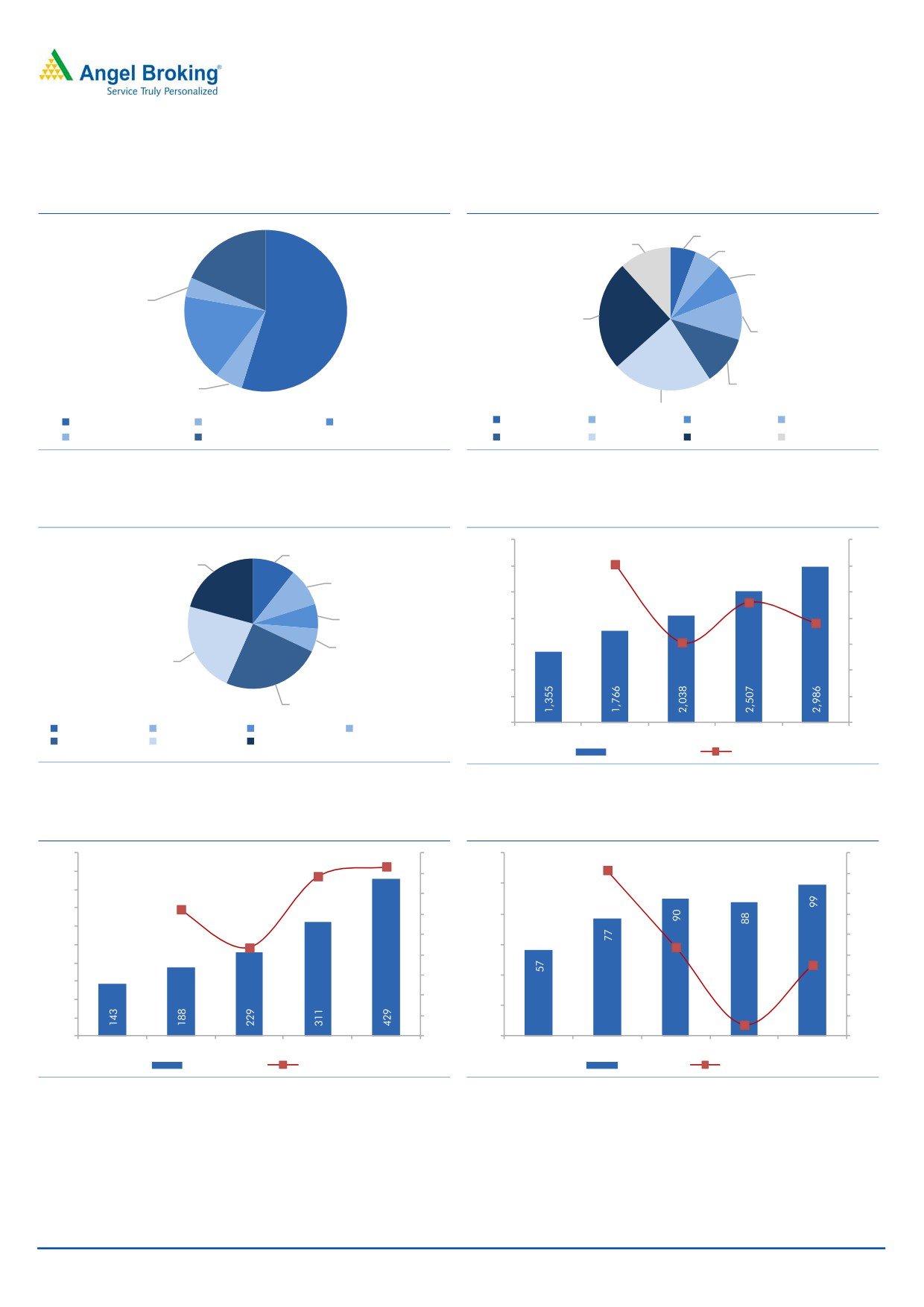

Exhibit 1: Order Inflow to catch-up

Exhibit 2: Execution to pick-up

3,000

200

3,500

1.8x

1.6x

1.6x

3,000

2,500

152

150

1.4x

2,500

2,000

1.2x

1.2x

100

2,000

1.0x

84

1.0x

1,500

0.9x

1,500

0.9x

0.8x

47

50

0.6x

1,000

0.6x

0.6x

1,000

0.5x

7

12

0.4x

0

500

(14)

500

0.2x

(32)

0

-50

0

0.0x

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

OI (` cr)

y/y change (%)

OB (` cr)

Execution Rate (x)

Source: Company, Angel Research

Source: Company, Angel Research

MBL’s unexecuted order book (as of 2QFY2015-end) stands at `2,354cr, thereby

giving revenue visibility for another 4-5 quarters. As against the Management’s

guidance of an order book of over `3,500cr by 4QFY2015-end, we expect MBL to

end with an order book of `2,886cr. Our lower OB assumption for FY2015 is

owing to expectation of just `1,700cr of OI for FY2015 (to-date, publicly reported

OI of `860cr). However, with order inflow momentum likely to catch-up from

here-on, we expect MBL to also experience strong uptick in execution (execution

rate would pick-up from 0.6x in FY2014 to 1.0x by FY2017E).

January 23, 2015

2

Initiating coverage | MBL Infrastructure

BOT projects to start paying-off

Currently, only 1 of the 5 BOT Road projects owned by MBL is operational. The

remaining 4 projects are likely to commence operations in FY2016-17E. 3 of the

4 ongoing projects are nearing completion (entire land acquisition is complete,

and majority of equity infusion is done), indicating minimal execution risks from

here-on. These 3 BOT projects are likely to attain Commercial Operations Date

(CoD) over the next 2-4 quarters.

Exhibit 3: BOT Projects Net Total Income (in ` cr)

FY14

FY15E

FY16E

FY17E

Seoni-Balaghat-Rajegaon BOT project

17

19

21

23

Waraseoni-Lalbarra BOT project

0

0

8

12

Garra-Waraseoni BOT project

0

0

14

23

Seoni-Katangi BOT project

0

0

11

22

Suratgarh-Bikaner BOT project

0

0

0

50

BOT Projects - Net Total Income

17

19

54

130

Source: Company, Angel Research

Given that the ongoing EPC work at Suratgarh-Bikaner BOT project is slow and

behind schedule (~20% of total EPC work is done), we expect this project to attain

CoD in 2HFY2017E.

AAP Infrastructures Ltd (Seoni-Balaghat-Gondia stretch), the company’s only

operational BOT project, has been profitable since FY2010 (incurred losses during

FY2008-09). Notably,

2 of the

4 BOT projects have been bagged under

Toll+ Annuity model and another 2 have been bagged on a grant model. We are

impressed with Management’s business acumen, as MBL is likely to generate

Future Cash flows of 0.4x-2.5x for the equity invested. MBL’s cautious strategy

impresses us as in our view, we expect MBL to generate impressive Equity IRRs in

the range of

15-18% (for

3 of the upcoming BOT projects). Whereas,

Garra-Waraseoni project in our view is likely to generate just 6% equity IRR.

We expect MBL’s Net Total Income from BOT projects to increase from `17cr in

FY2014 to `130cr in FY2017E (95% CAGR during FY2014-17E). Also, with the

commencement of tolling across 4 BOT projects, we expect the debt repayment

cycle of these SPVs to commence, thereby easing consol. balance sheet stress.

~18% & ~16% Revenue & PAT CAGR, respectively, during FY14-17E

On the back of a strong ~13% CAGR in Order Inflows during FY2014-17E, we

expect execution also to pick. Accordingly, we expect the standalone business to

report ~18% revenue CAGR during FY2014-17E to `2,857cr.

Revenue growth should help MBL absorb fixed costs, leading to EBITDA growth.

Our 22% EBITDA CAGR estimate during FY2014-17E is on the back of following

levers, (1) benefits from their in-house Ready-To-Mix concrete (RMCs), (2) access to

6 quarrying facilities, (3) higher utilization of in-house Construction Equipment

(current Plant & Machinery [P&M] Gross block stands at `200cr), and (4) better

absorption of fixed costs. Despite commencement of interest rate down-cycle, we

do not expect entire benefits of EBITDA growth to flow-down to the PAT level. We

expect interest and depreciation expenses to restrict PAT CAGR during FY2014-17E

to ~16%.

January 23, 2015

3

Initiating coverage | MBL Infrastructure

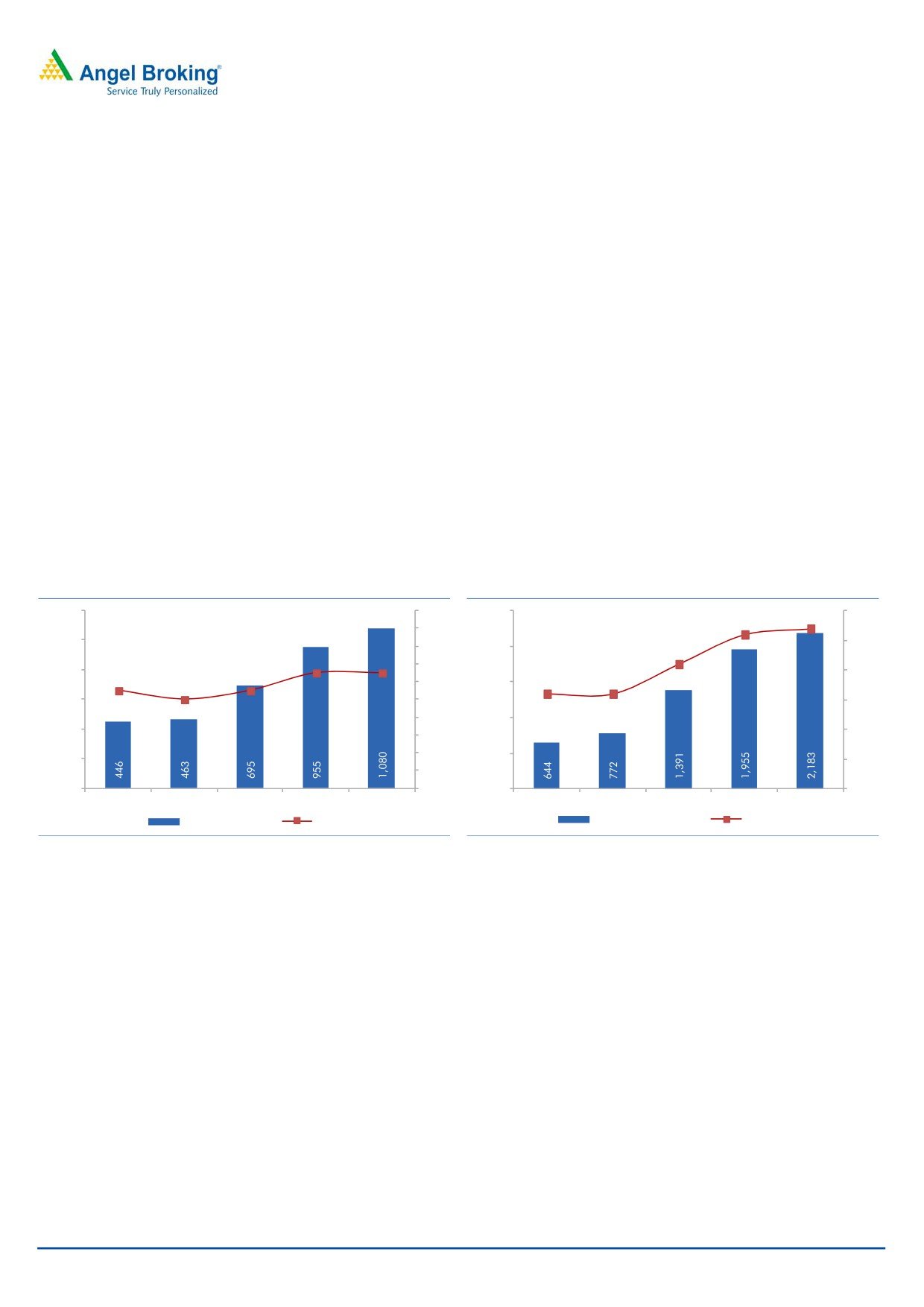

Comfortable Gearing ratio

MBL has been prudent in managing its capital requirements. Considering

standalone entity’s D/E ratio (of ~1.0x) and standalone entity’s potential to

generate over `100cr of Cash Flow from Operations during FY2014-17E, we are

not much concerned about the gearing ratio at standalone entity level.

MBL’s selective strategy to bid for and win new BOT projects at the right time has

helped the company in managing its capital efficiently. This could be gauged from

their consol. D/E ratio, which at 2QFY2015-end stood at 1.8x.

As a prudent move, in anticipation of improvement in business cycle, MBL recently

pursued a Qualified Institutional Placement (QIP) issue (issued 3.2mn additional

shares @`365/share, thereby raising ~`110cr). 4 of the ongoing BOT projects

require equity investments of ~`87cr. With MBL’s Management clarifying that it

would not bid for BOT Road projects till FY2017E, idly lying cash and internal

accruals should be enough to fund the equity requirements of these 4 BOT

projects. Also, by raising equity, MBL has built-up its war chest for the next phase

of growth. On the whole, we expect consol. gearing ratio to increase to 2.7x by

FY2017E, which is in a comfortable zone.

Exhibit 4: Standalone D/E ratio

Exhibit 5: Consolidated D/E ratio

1,200

2.0x

2,500

3.0x

2.7x

1.8x

2.6x

1,000

2.5x

1.6x

2,000

1.3x

1.4x

2.1x

800

1.3x

2.0x

1.2x

1,500

1.1x

1.6x

1.1x

1.0x

1.6x

600

1.0x

1.5x

0.8x

1,000

400

1.0x

0.6x

0.4x

500

200

0.5x

0.2x

0

0.0x

0

0.0x

FY13

FY14

FY15E

FY16E

FY17E

FY13

FY14

FY15E

FY16E

FY17E

Std. Debt (` cr)

D/E ratio (x)

Consol. Debt (` cr)

D/E ratio (x)

Source: Company, Angel Research

Source: Company, Angel Research

Selective bidding, best approach to grow Order Book

MBL, over the years, has shown immense maturity in bidding for the right kind of

projects and working for clients who are quality conscious. It bids for projects,

which are funded either by government agencies or international bodies such as

World Bank and ADB. This strategy mitigates payment default risk and helps

maintain WC levels prudently.

When the entire industry was witnessing heated competition and experiencing

higher D/E ratios (on account of higher exposure to BOT road projects), MBL

stayed away from the BOT space. It was only after competition started easing-off

that MBL entered the BOT Road space. This strategy helped them bid for projects

in a lesser competitive environment and sign the projects with attractive terms.

Given that 2 of MBL’s projects are on Toll+ Annuity and another 2 on Toll+ Grant

model, we are optimistic of the company experiencing impressive equity IRR across

these projects. This strategy has also helped MBL in building its order book in a

down-cycle, when the award activity witnessed severe slowdown. It is this business

January 23, 2015

4

Initiating coverage | MBL Infrastructure

prudence, which helped MBL cover its fixed costs base in a down-cycle and

maintain ~10% standalone EBITDA levels.

Notably, all projects of MBL have a price pass-on clause in-built, thereby insulating

the company from any sharp fall in EBITDA margins.

All the above-mentioned initiatives and well timed strategic moves have helped

MBL maintain ~10% EBITDA margins during FY2010-14 and generate Cash flow

from Operations to the tune of ~`176cr during FY2012-14.

Backward integration to aid in quicker margin expansion

MBL over the years has invested in (1) Ready-to-Mix Concrete (RMC) plants,

(2)

6 quarrying facilities strategically located across North & Eastern India and

(3) wide array of Construction Equipments. This strategy to invest in resources

would help the company in ensuring quick and timely supply of stone aggregates

at the project location, thus translating into cost savings. In an up-cycle, where

award activity is likely to see a sharp bounce back, we expect having large

inventory of construction equipments would help MBL in lowering execution costs;

reduce mobilization time, thereby translating to higher operating margins. All

these backward integration initiatives should help the standalone entity in reporting

a 107bp EBITDA margin expansion during FY2014-17E to 11.1%.

January 23, 2015

5

Initiating coverage | MBL Infrastructure

Update on BOT Projects

MBL has a portfolio of 5 BOT Road projects, of which only 1 is operational

(Seoni-Balaghat-Gondia). MBL’s Management has guided that all 4 BOT road

projects would be operational in FY2016E (vs. our assumption of only 3 being

operational in FY2016E). By 2QFY2015-end, MBL had already invested `201cr of

the total required `288cr, implying that `87cr further needs to be invested towards

these 4 BOT projects. ~`110cr raised from the QIP issue and internal accruals

should help MBL meet the remaining equity requirement of `87cr.

Exhibit 6: Details of BOT Projects

Particulars

AAPIL

MHDCL

MPTRCL

MPRNCL

SBTRCL

Seoni-Balaghat-

Waraseoni-

Garra-

Stretch

Seoni-Katangi

Bikaner-Suratgarh

Gondia

Lalbarra Road

Waraseoni

Project Type

BOT- Toll

BOT- Toll

BOT- Toll+Annuity

BOT- Toll+Annuity

BOT- Toll

State

Madhya Pradesh

Maharashtra

Madhya Pradesh

Madhya Pradesh

Rajasthan

Length (kms)

114

76

18

47

172

Status

Operational

Under Construction Under Construction Under Construction Under Construction

Concession Period

15 years

30 years

15 years

15 years

16 years

MBL's stake

100%

100%

100%

100%

65%

Concession Agreement Date

Mar-05

Sep-11

Dec-11

Mar-13

Dec-11

TPC (` in cr)

108

212

57

137

620

EPC (` in cr)

91

177

47

110

510

Debt (` in cr)

61

101

42

97

450

Equity (` in cr)

12

51

15

40

170

Grant (` in cr)

35

60

0

0

0

Traffic Growth Assumption:

1-5 years

5%

5%

5%

5%

6-16 years

5%

3%

3%

3%

3%

16 years and there-after

0%

NA

NA

NA

Equity IRR (%)

15%

16%

6%

18%

Source: Company, Angel Research; Note: NA- Not Applicable

MBL’s Management maintained that they have strategically bid for road projects in

mineral rich regions, which also happen to be important hubs and presently do not

have any other alternative connecting roads. Notably, 4 of the 5 BOT road

projects are inter-connected namely, Seoni- Balaghat-Gondia, Seoni-Katangi to

Maharashtra Border, Waraseoni-Lalbarra and Garra-Waraseoni stretches.

Accordingly, MBL’s Management claims to have 2 stretches of BOT projects. One

of the stretches is on NH-15 across Suratgarh-Bikaner (connecting north India to

Samakhiali, Gujarat) and other one is a stretch across NH-6/7 in Madhya

Pradesh.

January 23, 2015

6

Initiating coverage | MBL Infrastructure

Consolidated Financials

MBL reported an impressive 29% top-line CAGR during FY2010-14 to `1,766cr.

This top-line growth reflects (1) ~51% order book CAGR during the same period,

and (2) ~21% Toll Income CAGR during same period (for their only operational

BOT- Seoni-Balaghat-Rajegaon stretch). At 2QFY2015E-end, MBL’s unexecuted

order book stood at `2,354cr, thereby giving revenue visibility for another

4-5 quarters. For 1HFY2015E, MBL reported a 14.0% yoy top-line growth (to

`864cr). With uptick in order book and commencement of 4 BOT road projects,

we expect MBL to report a 19% top-line CAGR during FY2014-17E.

Exhibit 7: Consol. Revenue split

FY14-17E

Particulars (` cr)

FY14

FY15E FY16E

FY17E

CAGR (%)

Consolidated Revenues

1,766

2,038

2,507

2,986

19

Standalone Revenues

1,749

2,019

2,453

2,857

18

Revenues from BOT Projects

17

19

54

130

95

Seoni-Balaghat-Rajegaon BOT project

17

19

21

23

10

Waraseoni-Lalbarra BOT project

0

0

8

12

n/a

Garra-Waraseoni BOT project

0

0

14

23

n/a

Seoni-Katangi BOT project

0

0

11

22

n/a

Suratgarh-Bikaner BOT project

0

0

0

50

n/a

Source: Company, Angel Research; Note: n/a- Not Applicable

Despite a challenging macro environment, EPC business’ dependency on captive

BOT projects helped the company maintain its EBITDA margins at over 10% levels.

During FY2010-14, MBL reported an impressive 19.6% EBITDA CAGR (to `188cr).

With 4 of the BOT projects (have higher EBITDA margins vs. EPC business) likely to

commence operations in FY2016-17, coupled with (1) efficiencies from their

backward integration initiatives, and (2) new project wins on low bidding intensity,

we can expect MBL to report sharp EBITDA growth during FY2014-17E (we have

modeled ~32% CAGR over FY2014-17E). In other words, we expect EBITDA

margins to expand by 372bp during FY2014-17E to 14.4%.

Exhibit 8: Consol. EBITDA split

FY14-17E

Particulars (` cr)

FY14

FY15E FY16E FY17E

CAGR (%)

Consolidated EBITDA

188

229

311

429

32

Standalone EBITDA

176

212

267

317

22

BOT Projects EBITDA

12

17

44

112

111

Source: Company, Angel Research

During FY2010-14, MBL reported a restricted PAT CAGR of ~9%, reflecting the

impact of higher interest and depreciation expenses (partly owing to their

Seoni-Balaghat-Rajegaon BOT project). 4 of the BOT projects are expected to

commence operations in FY2016-17E. We do not expect the entire benefits of

EBITDA growth to flow down to the PAT level, as interest and depreciation

expenses would also increase. Accordingly, we expect MBL to report ~9% PAT

CAGR during FY2014-17E. In other words, PAT margins would decline from 4.4%

in FY2014 to 3.3% by FY2017E.

January 23, 2015

7

Initiating coverage | MBL Infrastructure

Exhibit 9: Consol. PAT split

FY14-17E

Particulars (` cr)

FY14A

FY15E

FY16E

FY17E

CAGR (%)

Consolidated PAT

77

90

88

99

9

Standalone PAT

75

85

100

118

16

BOT Projects PAT

2

5

(12)

(19)

NA

Source: Company, Angel Research; Note: NA - Not applicable

Capital deployment towards BOT projects, which report losses in first 1-2 years,

should be a drag on overall return ratios of the company. Accordingly, we expect

consol. Return on Capital Employed (RoCE) and Return on Equity (RoE) ratios to

decline from ~16%/18% in FY2014 to ~13%/13% in FY2017E.

Exhibit 10: Consolidated RoCE (%)

Exhibit 11: Consolidated RoE (%)

18

20

16

18

14

16

14

12

12

10

10

8

8

6

6

4

4

2

2

0

0

FY13

FY14

FY15E

FY16E

FY17E

FY13

FY14

FY15E

FY16E

FY17E

Source: Company, Angel Research

Source: Company, Angel Research

January 23, 2015

8

Initiating coverage | MBL Infrastructure

Valuation

We have valued MBL using Sum-Of-The-Parts method. MBL’s EPC business (under

standalone entity) has been valued using FY2017E P/E multiple, whereas BOT

projects are valued using the “Free Cash flow to Equity holders” method.

Value of Core EPC business

The standalone EPC business is trading at FY2016E and FY2017E P/E multiple of

9.1x and 7.8x, respectively. Standalone entity EPC is trading at ~25% discount to

its peers’ average (include- Simplex Infra, Ahluwalia Contracts, KNR Construction

and J Kumar Infra). This discount could be attributable to (1) MBL’s lower RoE of

14.8% for FY2017E vs. peers’ average of 16.3% in FY2017E), and (2) higher

dependency on only one vertical, i.e. the Roads Vertical (a/c’s for ~73% of

unexecuted order book).

Exhibit 12: Peer Group comparison (Standalone numbers)

Revenues (` cr)

EBITDA Margins (%)

PAT Margins (%)

Rev. CAGR

PAT CAGR

Particulars

FY14

FY15

FY16

FY17

FY15E FY16E FY17E FY15E FY16E FY17E

FY2014-17E(%)

FY2014-17E(%)

MBL Infra

1,754

2,019

2,453

2,857

10.5

10.9

11.1

4.2

4.1

4.1

17.7

16.3

Simplex Infra

5,499

5,696

6,472

7,670

10.7

10.8

10.4

1.2

1.8

2.6

11.7

49.4

KNR Construction

837

886

1,059

1,336

15.4

15.5

14.7

7.1

7.3

7.3

16.9

17.2

Ahluwalia Contracts

957

1,155

1,408

1,692

10.3

11.0

11.9

5.7

6.2

7.0

20.9

76.0

J Kumar Infra

1,169

1,456

1,774

2,191

17.5

17.3

16.8

6.9

7.4

7.6

23.3

25.9

Average

13.5

13.7

13.5

5.2

5.7

6.2

18.2

42.1

Source: Bloomberg estimates, Company, Angel Research

Exhibit 13: Peer Group comparison (Standalone numbers)

M-Cap

RoE (%)

EPS (`)

Adj. P/E (x)

CMP

(` cr)

FY14

FY15

FY16

FY17

FY15E

FY16E

FY17E

FY15E

FY16E

FY17E

MBL Infra

442

916

17.6

15.2

14.4

14.8

40.9

48.5

57.0

10.7

9.0

7.7

Simplex Infra

366

1,812

4.5

4.9

7.8

12.1

13.9

24.1

41.7

26.3

15.2

8.8

KNR Construction

378

1,055

4.5

4.9

7.8

12.1

22.3

27.5

34.9

16.8

13.6

10.8

Ahluwalia Contracts

243

1,626

10.1

23.1

23.2

24.4

10.1

13.4

17.9

24.1

18.1

13.5

J Kumar Infra

476

1,535

15.6

14.9

16.0

16.8

31.9

41.6

52.0

14.9

11.4

9.2

Average

8.7

12.0

13.7

16.3

20.5

14.6

10.6

Source: Bloomberg estimates, Company, Angel Research

We have valued MBL’s core EPC business (standalone entity) based on P/E multiple

and assigned 8.0x for FY2017E EPS of `57, resulting in value of `456 per share.

Value of BOT projects

BOT projects have been valued using the “Free Cash flow to Equity holders”

method. Our value for all the 5 BOT projects comes to `105/share, which is 19%

January 23, 2015

9

Initiating coverage | MBL Infrastructure

of the overall SOTP value for the company. Ongoing projects contribute 3% and

under-development projects contribute 16% to the overall value.

On combining the value of EPC business BOT projects, we arrive at a combined

business value of `561/share, reflecting 27% upside in the stock price from the

current levels. In order words, the stock’s current market price reflects the business

value of just the standalone entity. We sense that as and when announcements of

the remaining

4 BOT projects are made, the stock price would catch-up

accordingly. We initiate coverage on MBL with a target price of `561/ share.

Exhibit 14: Sum-of-the-Parts based Valuation Table

FY17E Std. PAT

Target Value

Value/ share

Particulars

Segment

Target Multiple

% of SoTP Basis

(` cr)

(` cr)

(`)

MBL's EPC business

Construction

118

8.0

945

456

81

P/E of 8.0x

Total

945

456

81

Discounted FCFE

Adj. FCFE Value

Value/ share

Particulars

Proj. Type

Project Stake

% of SoTP Basis

(` cr)

(` cr)

(`)

Road BOT projects

Seoni-Balaghat-Rajegaon

Toll

31

100%

31

15

3

Ke of 17%

BOT Project

Waraseoni-Lalbarra BOT Project Toll + Annuity

22

100%

22

11

2

Ke of 17%

Garra-Waraseoni BOT Project Toll + Annuity

17

100%

17

8

1

Ke of 17%

Seoni-Katangi BOT Project

Toll

74

100%

74

36

6

Ke of 17%

Suratgarh-Bikaner BOT Project

Toll

114

65%

74

35

6

Ke of 17%

Total

258

218

105

19

Grand Total

1,162

561

100

Upside

27%

CMP

442

Source: Company, Angel Research

Key risks

Promoters have pledged ~5% of their equity stake (Promoters hold 46% stake

in MBL Infra). Any further increase in the pledge by the promoters could lead

to volatility in the stock price.

Suratgarh-Bikaner BOT project currently accounts for ~20% of unexecuted

order book. Any further delays in getting clearances could impact our near-

term execution assumptions, as well as equity IRRs.

Lower than expected order inflows due to slowdown in new project award

activity

Slower growth vs. our traffic growth expectations is potential risk to toll

revenues from BOT projects.

January 23, 2015

10

Initiating coverage | MBL Infrastructure

Exhibits

Exhibit 15: Order Book split- Vertical-wise

Exhibit 16: Order Book split- State-wise

5.8%

11.7%

6.0%

18.3%

7.2%

3.9%

24.9%

17.5%

54.8%

10.7%

11.1%

5.5%

22.6%

Roads & Highway Cons. Railway Infra

Building & Housing

Haryana

Assam

New Delhi

Uttarakhan

Other Infra

Roads & Highway O&M

West Bengal

Rajasthan

Madhya Pradesh Others

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 17: Order Book split- Client-wise

Exhibit 18: Consol. Revenue (` cr)

35

3,500

10.7%

20.8%

3,000

30

30

9.5%

2,500

25

23

6.1%

2,000

20

19

5.8%

1,500

15

15

22.6%

1,000

10

500

5

24.6%

0

0

PWD Uttarakhand WBHDCL

NHAI

PWD Haryana

Others

PWD Rajasthan

MPRDC

FY13

FY14

FY15E

FY16E

FY17E

Revenues (` cr)

y/y change (%)

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 19: Consol. EBITDA (` cr)

Exhibit 20: Consol. PAT (` cr)

500

45

120

40

42

450

40

36

35

39

100

400

35

30

350

31

30

80

25

300

22

25

20

250

60

17

20

15

200

13

15

40

10

150

10

5

100

20

50

5

-

(2)

0

0

0

(5)

FY13

FY14

FY15E

FY16E

FY17E

FY13

FY14

FY15E

FY16E

FY17E

EBITDA (` cr)

y/y change (%)

PAT (` cr)

y/y change (%)

Source: Company, Angel Research

Source: Company, Angel Research

January 23, 2015

11

Initiating coverage | MBL Infrastructure

Exhibit 21: Standalone Return on Equity (%)

Exhibit 22: Standalone Return on Capital Employed (%)

20

20

18

20

16

19

14

19

12

18

10

18

8

17

6

17

4

16

2

16

0

15

FY13

FY14

FY15E

FY16E

FY17E

FY13

FY14

FY15E

FY16E

FY17E

Source: Company, Angel Research

Source: Company, Angel Research

January 23, 2015

12

Initiating coverage | MBL Infrastructure

Exhibit 23: List of Ongoing projects

Contract Value

Unexecuted Value

Project details

(` in cr)

(` in cr)

Development & Operation on BOT basis of Bikaner-Suratgarh of NH-15

510

411

Widening to 4-lane of Dankuni-Chandanagar section of SH-13

318

275

Improve & strengthening of roads under Package no. C-4 in Almora dist.

217

217

Construction of Seoni-Katangi BOT Road project

177

21

RCD Contract, ADB funded project for improvement/ upgradation of roads & bridges of SH-68

169

37

(Shivganj-Rafiganj- Uphara-Devkund-Baidrabad)

NHAI contract to widen-strengthen NH-37 stretch of Sonapur-Guwahati (51% JV with TCIL)

158

40

Improve & strengthen roads under Package no. C-2 in Udham singh Nagar dist.

143

143

Construction of Garra-WaraSeoni BOT Road project

110

59

Construct buildings at National Law University, Rajiv Gandhi Education City, Sonepat Dist.

92

91

Construct depot-cum-workshop at Kalindi-kunj (Line-8 for Delhi MRTS Phase III)

84

56

Construct 222 flats, Keelandev Towers at Shivaji Nagar, Bhopal, MP

63

48

Construct Bus Terminus at GT Road, Serampore Municipality, Hooghly, WB

55

39

Re-development of Police Colony, Delhi Cantt.

50

47

Construction of Residential Buildings for NHAI staff at Dwarka, N-Delhi

49

19

Construction of WaraSeoni-Lalbarra BOT Road project

47

6

Construct Assam Judicial Academy & National Law School at Amingaon, Assam

44

32

Construct 4-lane RoB at Delhi Ambala line in Sonepat, Haryana

43

20

Construct Police Residence Quarters at Kindli Check Post, Delhi

41

19

Construct 96 flats at Tulsi Nagar, Bhopal

40

32

Construct 2-lane RoB at Delhi Ambala Railway line of Sonepat-Purkhas Road, Sonepat, Haryana

36

27

Construct Group Housing Residential Apartments for NBCC on Delhi Saharanpur Highway, Baghpat, UP

35

1

Construct 92 flats at Mahadev Parisar, & Construct Commercial Building at Shivaji Nagar, Bhopal

24

7

Construct 2-lane RoB at Delhi Ambala Railway line of Delhi-Ambala, Sonepat, Haryana

23

1

Construct Panchayat & Rural Development Dept. Building at Sector-19 in Naya Raipur

19

17

Construct Police Station & Residences at Hari Nagar, New Delhi

19

10

Construct Residential Accommodation for Senior Officers of SPA, Bhopal

13

11

O&M of Garra-Waraseoni Road project

38

38

O&M of Waraseoni-Lalbarra Road project

15

15

O&M of Seoni-Katangi Road project

263

263

O&M of Suratgarh-Bikaner Road project

251

251

O&M of Seoni-Balaghat Gondia Road, MP

51

49

Residential Complex for Judicial staff at Sec-19, Dwarka, Delhi

46

46

Other Contracts

85

8

Total Gross Order Book

3,327

2,354

Source: Company, Angel Research

January 23, 2015

13

Initiating coverage | MBL Infrastructure

Income Statement (Standalone)

Y/E March (` cr)

FY13

FY14

FY15E

FY16E

FY17E

Net Sales

1,343

1,754

2,019

2,453

2,857

% Chg

30.6

15.1

21.5

16.5

Total Expenditure

1,211

1,578

1,807

2,186

2,539

Cost of Materials Consumed

954

1,376

1,587

1,921

2,237

Direct Labour, Sub-Contracts

180

118

125

150

173

Employee benefits Expense

23

27

30

39

44

Other Expenses

55

57

65

76

86

EBITDA

131

176

212

267

317

% Chg

34.0

20.3

26.1

18.7

EBIDTA %

9.8

10.0

10.5

10.9

11.1

Depreciation

7

10

15

19

21

EBIT

124

166

197

249

296

% Chg

33.9

18.3

26.4

19.0

Interest and Financial

51

70

84

115

139

Charges

Other Income

1

4

2

3

3

PBT

74

101

115

136

160

Tax

19

26

30

35

42

% of PBT

25.4

25.4

26.0

26.0

26.0

PAT before Exceptional item

55

75

85

100

118

Exceptional item

0

0

0

0

0

PAT

55

75

85

100

118

% Chg

35.8

12.9

18.4

17.6

PAT %

4.1

4.3

4.2

4.1

4.1

Diluted EPS

32

43

41

48

57

% Chg

35.8

(4.6)

18.4

17.6

January 23, 2015

14

Initiating coverage | MBL Infrastructure

Balance Sheet (Standalone)

Y/E March (` cr)

FY13

FY14

FY15E

FY16E

FY17E

Sources of Funds

Equity Capital

18

18

21

21

21

Reserves Total

374

443

633

725

833

Networth

391

460

654

746

854

Total Debt

446

463

695

955

1,080

Other Long-term Liabilities

108

153

199

199

199

Deferred Tax Liability

30

34

35

35

35

Total Liabilities

974

1,111

1,582

1,934

2,167

Application of Funds

Gross Block

175

214

279

324

364

Accumulated Depreciation

38

48

63

81

102

Net Block

137

166

216

243

261

Capital WIP

0

0

0

0

0

Investments

98

166

220

308

308

Current Assets

Inventories

491

559

729

872

984

Sundry Debtors

302

374

544

640

730

Cash and Bank Balance

18

13

18

51

98

Loans, Advances & Deposits

71

97

90

89

95

Other Current Asset

4

6

39

46

48

Current Liabilities

285

324

365

405

447

Net Current Assets

601

725

1,056

1,294

1,508

Other Assets

139

53

90

90

90

Total Assets

974

1,111

1,582

1,934

2,167

January 23, 2015

15

Initiating coverage | MBL Infrastructure

Cash Flow Statement (Standalone)

Y/E March (` cr)

FY13

FY14

FY15E

FY16E

FY17E

Profit before tax

74

101

115

136

160

Depreciation

7

10

15

19

21

Change in Working Capital

(80)

(3)

(308)

(205)

(168)

Interest & Financial Charges

51

70

84

115

139

Direct taxes paid

(47)

(14)

(30)

(35)

(42)

Cash Flow from Operations

5

163

(125)

30

111

(Inc)/ Dec in Fixed Assets

(33)

(39)

(65)

(45)

(40)

(Inc)/ Dec in Investments

(26)

(68)

(54)

(88)

-

Cash Flow from Investing

(59)

(107)

(119)

(133)

(40)

Issue/ (Buy Back) of Equity

-

-

117

-

-

Inc./ (Dec.) in Loans

109

18

232

260

125

Dividend Paid (Incl. Tax)

(3)

(6)

(9)

(9)

(10)

Interest Expenses

(51)

(70)

(84)

(115)

(139)

Cash Flow from Financing

55

(58)

256

136

(24)

Inc./(Dec.) in Cash

1

(3)

13

33

46

Opening Cash balances

7

8

6

18

51

Closing Cash balances

8

6

18

51

98

January 23, 2015

16

Initiating coverage | MBL Infrastructure

Key Ratio (Standalone)

Y/E March

FY13

FY14

FY15E

FY16E

FY17E

Valuation Ratio (x)

P/E (on FDEPS)

14.0

10.3

10.8

9.1

7.8

P/CEPS

12.4

9.1

9.2

7.7

6.6

Dividend yield (%)

0.7

0.7

0.8

0.8

0.9

EV/Sales

0.9

0.7

0.8

0.7

0.7

EV/EBITDA

9.2

7.0

7.5

6.8

6.0

EV / Total Assets

1.2

1.1

1.0

0.9

0.9

Per Share Data (`)

EPS (fully diluted)

31.6

42.9

40.9

48.5

57.0

Cash EPS

35.7

48.5

48.3

57.5

67.3

DPS

3.0

3.0

3.7

3.5

4.2

Book Value

224

263

315

360

412

Returns (%)

RoCE (Pre-tax)

16.6

19.3

17.5

16.5

16.5

Angel RoIC (Pre-tax)

15.0

18.4

14.7

14.8

15.5

RoE

15.1

17.6

15.2

14.4

14.8

Turnover ratios (x)

Asset Turnover (Gross Block) (X)

0.8

0.9

0.9

0.9

0.9

Inventory / Sales (days)

134

109

116

119

119

Receivables (days)

82

70

83

88

88

Payables (days)

28

27

25

22

20

Leverage Ratios (x)

D/E ratio (x)

1.1

1.0

1.1

1.3

1.3

Interest Coverage Ratio (x)

2.4

2.4

2.4

2.2

2.1

January 23, 2015

17

Initiating coverage | MBL Infrastructure

Income Statement (Consolidated)

Y/E March (` cr)

FY13

FY14

FY15E

FY16E

FY17E

Net Sales

1,355

1,766

2,038

2,507

2,986

% Chg

30.3

15.4

23.0

19.1

Total Expenditure

1,212

1,578

1,809

2,196

2,557

Cost of Materials Consumed

954

1,376

1,587

1,921

2,237

Direct Labour, Sub-Contracts

180

118

125

150

173

Employee benefits Expense

23

27

30

39

44

Other Expenses

55

57

67

87

103

EBITDA

143

188

229

311

429

% Chg

31.2

21.6

35.8

38.1

EBIDTA %

10.6

10.7

11.2

12.4

14.4

Depreciation

11

14

21

34

57

EBIT

132

174

208

277

372

% Chg

31.6

19.4

33.3

34.3

Interest and Financial Charges

58

75

89

155

246

Other Income

2

4

2

3

3

PBT

76

103

121

125

129

Tax

20

26

31

36

44

% of PBT

25.7

25.2

25.3

29.2

33.9

PAT before Exceptional item

57

77

90

88

85

Exceptional item

0

0

0

0

0

PAT before Minority Interest

57

77

90

88

85

Minority Interest

0

0

0

0

(14)

PAT after Minority Interest

57

77

90

88

99

% Chg

35.9

17.1

(1.9)

12.2

PAT %

4.2

4.4

4.4

3.5

3.3

Diluted EPS

32

44

43

43

41

% Chg

36.0

(1.1)

(1.9)

(3.8)

January 23, 2015

18

Initiating coverage | MBL Infrastructure

Balance Sheet (Consolidated)

Y/E March (` cr)

FY13

FY14

FY15E

FY16E

FY17E

Sources of Funds

Equity Capital

18

18

21

21

21

Reserves Total

380

451

642

722

797

Networth

398

469

663

742

817

Total Debt

644

772

1,391

1,955

2,183

Other Long-term Liabilities

44

40

73

73

73

Minority Interest

0

32

32

32

18

Deferred Tax Liability

30

34

35

35

35

Total Liabilities

1,116

1,347

2,193

2,837

3,126

Application of Funds

Gross Block

248

287

352

841

1,583

Accumulated Depreciation

59

73

91

121

183

Net Block

189

214

261

720

1,400

Capital WIP

209

376

715

620

0

Investments

20

20

24

24

24

Current Assets

Inventories

491

559

729

872

984

Sundry Debtors

253

318

594

731

829

Cash and Bank Balance

77

68

15

50

102

Loans, Advances & Deposits

72

98

90

89

95

Other Current Asset

6

8

39

46

48

Current Liabilities

208

330

365

405

447

Net Current Assets

692

721

1,103

1,382

1,612

Other Assets

6

16

90

90

90

Total Assets

1,116

1,347

2,193

2,837

3,126

January 23, 2015

19

Initiating coverage | MBL Infrastructure

Cash Flow Statement (Consolidated)

Y/E March (` cr)

FY13

FY14

FY15E

FY16E

FY17E

Profit before tax

76

103

121

125

129

Depreciation

11

14

21

34

57

Change in Working Capital

(35)

(56)

(472)

(248)

(172)

Interest & Financial Charges

58

75

89

155

246

Direct taxes paid

(48)

(14)

(31)

(36)

(44)

Cash Flow from Operations

62

122

(272)

28

216

(Inc)/ Dec in Fixed Assets

(172)

(206)

(404)

(394)

(121)

(Inc)/ Dec in Investments

(20)

-

(4)

-

-

Cash Flow from Investing

(191)

(206)

(409)

(394)

(121)

Issue/ (Buy Back) of Equity

-

-

117

-

-

Inc./ (Dec.) in Loans

202

128

619

564

228

Dividend Paid (Incl. Tax)

(3)

(6)

(9)

(9)

(10)

Interest Expenses

(58)

(75)

(89)

(155)

(246)

Minority Interest

0

32

-

-

(14)

Cash Flow from Financing

142

78

638

401

(42)

Inc./(Dec.) in Cash

13

(6)

(42)

35

53

Opening Cash balances

50

63

57

15

50

Closing Cash balances

63

57

15

50

102

January 23, 2015

20

Initiating coverage | MBL Infrastructure

Key Ratio (Consolidated)

Y/E March

FY13

FY14

FY15E

FY16E

FY17E

Valuation Ratio (x)

P/E (on FDEPS)

13.7

10.1

10.2

10.4

10.8

P/CEPS

11.5

8.5

8.3

7.5

5.9

Dividend yield (%)

0.7

0.7

0.8

0.8

0.9

EV/Sales

1.0

0.8

1.1

1.1

1.0

EV/EBITDA

9.4

7.9

10.0

9.1

7.0

EV / Total Assets

1.2

1.1

1.0

1.0

1.0

Per Share Data (`)

EPS (fully diluted)

32.3

44.0

43.5

42.7

41.0

Cash EPS

38.7

52.0

53.6

58.9

75.3

DPS

3.0

3.0

3.7

3.5

4.2

Book Value

227.1

267.6

319.7

358.2

394.4

Returns (%)

RoCE (Pre-tax)

14.6

15.6

12.7

11.8

13.2

Angel RoIC (Pre-tax)

12.9

14.4

10.2

10.4

12.5

RoE

15.2

17.8

15.9

12.6

12.7

Turnover ratios (x)

Asset Turnover (Gross Block) (X)

0.6

0.7

0.7

0.5

0.4

Inventory / Sales (days)

127

108

115

117

113

Receivables (days)

57

59

82

97

95

Payables (days)

18

25

24

21

19

Leverage Ratios (x)

D/E ratio (x)

1.6

1.6

2.1

2.6

2.7

Interest Coverage Ratio (x)

2.3

2.4

2.4

1.8

1.5

January 23, 2015

21

Initiating coverage | MBL Infrastructure

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Angel Broking Pvt. Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavours to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Pvt. Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking

or other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or

in the past.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

MBL Infrastructure

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Returns):

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Reduce (-5% to -15%)

Sell (< -15%)

January 23, 2015

22

Initiating coverage | MBL Infrastructure

6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai- 400 093. Tel: (022) 39357800

Research Team

Fundamental:

Sarabjit Kour Nangra

VP-Research, Pharmaceutical

Vaibhav Agrawal

VP-Research (Banking)

Amarjeet Maurya

Analyst (FMCG, Media, Mid-Cap)

Bharat Gianani

Analyst (Automobile)

Rahul Dholam

Analyst (Metal, Oil & Gas)

Santosh Yellapu

Analyst (Infrastructure)

Shrenik Gujrathi

Analyst (Cap Goods, Cement)

Umesh Matkar

Analyst (Banking)

Twinkle Gosar

Analyst (Mid-Cap)

Tejas Vahalia

Research Editor

Technicals and Derivatives:

Siddarth Bhamre

Head - Technical & Derivatives

Sameet Chavan

Technical Analyst

Sneha Seth

Associate (Derivatives)

Institutional Sales Team:

Mayuresh Joshi

VP - Institutional Sales

Meenakshi Chavan

Dealer

Gaurang Tisani

Assistant Manager

Production Team:

Dilip Patel

Production Incharge

CSO & Registered Office: G-1, Ackruti Trade Centre, Road No. 7, MIDC, Andheri (E), Mumbai - 93. Tel: (022) 3083 7700. Angel Broking Pvt. Ltd: BSE Cash: INB010996539 / BSE F&O: INF010996539, CDSL Regn. No.: IN - DP - CDSL - 234 - 2004, PMS Regn. Code: PM/INP000001546, NSE Cash: INB231279838 /

NSE F&O: INF231279838 / NSE Currency: INE231279838, MCX Stock Exchange Ltd: INE261279838 / Member ID: 10500. Angel Commodities Broking (P) Ltd.: MCX Member ID: 12685 / FMC Regn. No.: MCX / TCM / CORP / 0037 NCDEX: Member ID 00220 / FMC Regn. No.: NCDEX / TCM / CORP / 0302.

January 23, 2015

23